Someone Is Getting Really Nervous About HP’s Debt

Shares of Hewlett-Packard hit another 52-week low yesterday, dropping to $18.30 and continuing their summer doldrums, trading in the lowest range they have seen in nearly eight years. The shares continued their depressing fall today, hovering below $18 in late trading and making another new low likely.

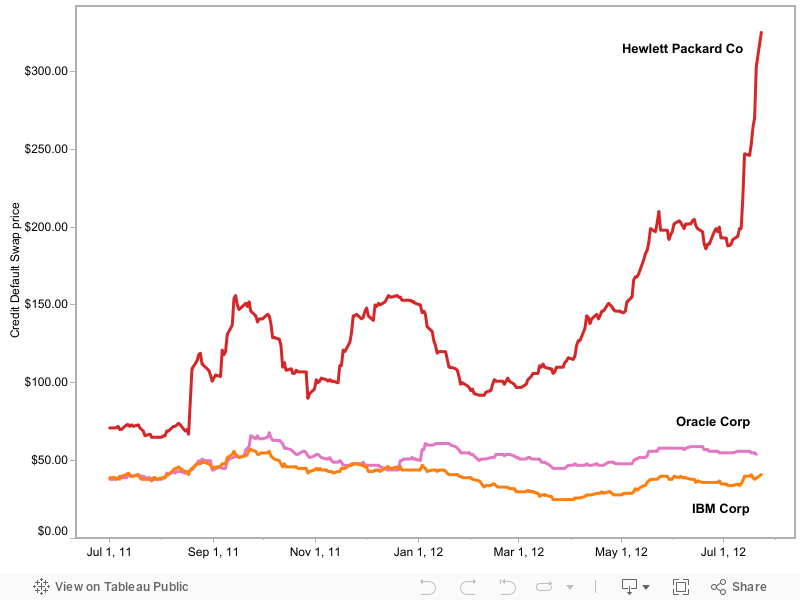

But another metric related to HP has in recent weeks started setting record highs. Prices on credit default swaps on HP’s debts have started to rise substantially, or, as pros in the corporate debt world like to say, “blow out.” The chart below shows the price progression since last July on credit default swaps for HP, IBM and Oracle, and you can see the striking disparity.

Now, without going too far into the weeds of corporate finance and debt (I wrote last month about the swelling debt on HP’s balance sheet), it’s important to understand what a credit default swap is and is not. Essentially, it’s insurance that you buy on a debt you hold to protect you against the possibility that the original debtor — in this case, HP — may default. The price of the swap was five times higher yesterday than it was at this time last year. As of yesterday, it cost $325,000 to insure $10 million of HP debt for five years, up from about $65,000 a year ago, according to data from Markit Group, which tracks the daily prices of credit default swaps.

It’s important to be clear on one point: No one is suggesting that HP is in any danger of defaulting on any of its debt. But for those holding HP bonds, the price of protection against that eventuality — however remote — is getting higher by the day.

And while the price of credit default swaps are mainly a barometer of the state of anxiety over its finances and its balance sheet, they can have the side effect of increasing the overall cost of HP’s financing activities and ultimately affecting its share price.

The pace in the increase of swap prices quickened last week following a perfect storm of bad news: There were lousy earnings reported by printing concerns Lexmark and Xerox, the apparent threat that HP may lose a key IT services contract at General Motors, and word that institutional investor James Chanos is shorting HP shares. The state of global PC sales in the second quarter and the disclosure that China’s Lenovo is drawing nearly even with market leader HP didn’t help.

Also consider this: HP has issued more than $10 billion worth of bonds reaching maturity in 2013 and 2014 on top of another billion and change maturing this year.

Typically, a company like HP can roll this debt over into new bonds relatively easily. But here’s the rub: HP’s credit ratings have slipped in recent months, increasing the cost of borrowing money generally. With less than a month to go before HP reports earnings for the quarter ending in July, no wonder people are getting nervous.

Note to the graph below: While the figures are given in dollars, the price is actually in hundreds of thousands of dollars. So yesterday’s price of $325 is actually $325,000, the spot price to buy protection against the loss of $10 million in debt.

(Thanks to AllThingsD’s Beth Callaghan for help with the chart and to The Wall Street Journal’s David Reilly for the quick lectures on the finer points of credit default swaps.)

{kind=link}