Why Zipcar’s “Greedy VCs” Weren’t Quick Enough

Avis is paying a 50 percent premium to buy up Zipcar. That’s good news for the car-sharing service, right?

Absolutely not, says managment guru Tom Peters. Via Twitter, he announced his disappointment:

Aargh. Hate hate hate to see Zipcar swallowed by Avis!! Greedy VCs looking for quick payback, I presume???

— Tom Peters (@tom_peters) January 2, 2013

After getting some pushback from start-up folk like First Round Capital’s Chris Fralic, kbs+’s Darren Herman and angel investor Jerry Neumann, Peters concedes that maybe this wasn’t the case here, and that he doesn’t really know or care much about Zipcar the company, but he really thinks most VCs suck.

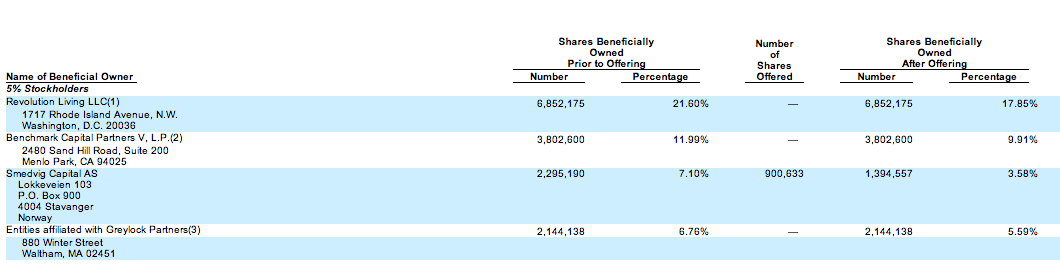

So let’s stipulate that some VCs are fantastic human beings and others are not. But let’s also point out that Zipcar’s three primary VC backers — Benchmark, Greylock and AOL co-founder Steve Case’s Revolution investment group — seem to have been Zipcar believers, not Zipcar flippers.

Zipcar went public in April 2011, when it priced at $18 a share and popped to $26. At the end of 2011, Benchmark still had 66 percent of its original stake, and Greylock and Case hadn’t sold a share (click charts to enlarge).

Neither Benchmark nor Greylock seem to have sold anything since then, while Case ended up betting $8 million more on Zipcar in August 2012.

Case’s summer investment now looks pretty good, since he was buying stock on the open market for an average of $7.80 a share, and Avis is going pay him $12.25. But Case, Greylock and Benchmark still missed many other chances to sell off their Zipcar stakes at much higher prices.

In November 2011 — more than half a year after the Zipcar IPO, when most lockups traditionally expire — Zipcar was trading at $20. If its VCs were looking for a quick payback, that would have been the best time to bail out.

{kind=link}