Stop Bashing the IPO Market — It’s Ripe for Recovery

Image copyright pupunkkop

The IPO is the lifeblood of our stock markets; it’s the vehicle that helps bring capital, liquidity and a sense of optimism to the U. S. economy. In the late 1990s, we had a market that was flush with technology-related IPOs. Today’s IPO market has been a series of stops and starts compared to then, and notably tainted by highly scrutinized, extremely volatile offerings.

While there have been recent successful IPOs like Eloqua, FleetMatics, Palo Alto Networks, ServiceNow, Splunk, Workday and Yelp, the investing public and the media are still skeptical. We keep seeing headlines like “The Other Tech IPO that Just Faltered,” “IPOs Remain Out of Kilter,” and “Lofty Gains Lift Gloom in IPO Market.” I have yet to talk to anyone who thinks much is going to change. It’s unfortunate, because I believe if you step back and look from a broad perspective, the elements are in place to bring the IPO pipeline closer to what it once was. It’s time to stop bashing it and look forward.

Throughout my years as a securities lawyer, investment banker and now venture capitalist, I have been intimately involved with over 100 initial public offerings. Most of them have been venture-backed companies in the technology sector. Many who have tracked my career would say I have worked on more technology IPOs than any other venture capitalist out there, with my first rodeo being with Four Phase Systems in 1975 all the way to FleetMatics, which went public in October.

I spent almost 20 years as a technology investment banker, eight of which were spent at Montgomery Securities, where I ran technology investment banking. It was there that I saw our IPO deal pipeline — at its peak — larger than Wall Street’s entire venture-backed company today. I came to this stark realization only recently, when I looked at a half-page sheet of upcoming public technology offerings from all the investment banking firms. It’s shocking to see. Our own deal sheet at Montgomery would always run onto a second page — and we were just one of the major firms at the time.

I am a firm believer that things can change. We can boost the pipeline of attractive offerings in today’s market by looking at it as a three-legged stool so that we start to fill more pages.

Three-Legged Stool Beneath the IPO Ecosystem

I view the IPO market as a three-legged stool that needs to be supported by a specific triad of parts to stay stable. Two of the three are already in place. The first leg is represented by a huge crop of strong attractive growth companies. The second is based on a favorable regulatory environment due to the recent passage of the Jumpstart our Business Startups (JOBS) Act. The third leg involves the investment banking system, which is the leg that needs adjustment. Once the three are aligned together, I believe the market can be ripe for recovery.

Leg No. 1: An Abundance of Venture-Backed Innovative Growth Companies

From what I am seeing right now, there are an incredible number of entrepreneurs creating compelling growth companies. While there were significantly more IPOs in the 1990s, the number of private companies currently being built is about five times what it was during that time. For example, in 1991, there were 319 venture investments in the core areas of the technology we know today. In 2011, there were 1,825. Yet there are far fewer IPOs.

Today’s entrepreneurs are defining massive, fast-growing markets that hardly existed 15 years ago, such as enterprise mobility, social marketing and big data analytics. They are also disrupting large established industries like travel, transportation and legal services. Compared to the 1990s, technology companies today have more sustainable, scalable models that can result in successful public companies in the long-term, where as we all know, only the strong will survive under the scrutiny of the public markets.

Companies today are vastly ahead of those I saw 20 years ago — stronger management teams, less capital intensive, bigger markets and better business models. An abundance of venture-backed innovative growth companies exists today. From this perspective, it is the best time ever. Therefore, the first leg of the stool is in full effect.

Leg No. 2: Favorable Regulatory Environment

Much of the previous regulatory clampdown (e.g., Sarbanes-Oxley and the Spitzer settlements) has been relieved under the JOBS Act. Now a smoother path exists to guide growth companies to go through the IPO process. This regulation has the potential to significantly affect the IPO process for smaller companies in a number of ways:

- Creating an IPO “on-ramp” for emerging growth companies (EGCs) with reduced SEC filing requirements

- Providing for realistic scaled disclosure, governance and accounting obligations for EGCs

- Relaxing restrictions on research analysts

- Allowing “testing of the waters”

- Allowing confidential IPO filings

Although there is now more flexibility, companies are not taking full advantage of the actions that are now allowed under the JOBS Act. While there are still some elements where the SEC needs to issue fuller guidelines, companies could be bolder and take advantage of the new laws.

Two of these areas — testing the waters and confidential IPO filings — are huge changes that companies should embrace. I’ll explain.

Testing the waters offers a huge advantage to young companies trying to gain an understanding of potential market reception. Historically, a company had to rely on feedback from its lead investment bankers as to what the likely reaction of the institutional buyer would be. While the bankers offer a reasonable proxy, they are far less informative than real life dry runs with a few institutional buyers. The bankers, having sold hard to get the business, have a natural optimistic bias and a tendency to support the company’s existing positioning. Testing of the waters is a terrific opportunity to explore the receptivity of the institutional buyer to the company, its positioning and target valuation. This can mitigate the risk of a disappointing or failed IPO. Amazingly, not everyone is doing this.

The confidential IPO filing is probably the most important change. Historically, EGCs were understandably concerned about showing their hand to competitors, suppliers and customers in an IPO filing unless they were quite sure that the IPO was going ahead. This created a certain caution by management teams. Now, companies can file confidentially and avoid these issues. They can get the clock rolling, work out any disclosure or accounting issues with the SEC, and only when they are ready to market the IPO do they need to show their hand. And this doesn’t preclude the “dual tracking” of an IPO and an M&A exit. A company can announce that it has filed even though the contents of the filing are still confidential. Nothing wrong with having your cake and eating it, too! The confidential IPO filing is a no-brainer that should be embraced and will allow companies to file that otherwise would have been on the fence and waiting.

Leg No. 3: The Investment Banking System

And now for the area in need of the most improvement: The investment banking ecosystem, which will require some changes and adjustment to reach its full potential and further drive our IPO pipeline.

The healthy IPO market of the 1990s was in large part created by the “Four Horsemen” of the technology investment banking world: Montgomery Securities, Hambrecht & Quist, Alex Brown and Robertson Stephens. Along with the well-known “Bulge Bracket” firms, those four boutique banks drove most of the technology IPO business during that period. These firms were small, nimble and not afraid to take risks. While those specific firms no longer exist and there have been many changes to the investment banking landscape, there is still top talent at both large and boutique growth-oriented investment banks.

Those people who have the skills and knowledge to bring value to growth companies exist today, and I can think of a number of firms fully qualified to be the next “Four Horsemen.” But even though we have the banks and the talent, the banking system still needs the economic incentive to get the banks more involved and motivated to bring companies public.

Currently, underwriting syndicates are being created in a way that dramatically limits the economic incentives to small firms. In the 1990s, the economics, or banking fees, were more favorably divided among the lead banks and the co-managers of the deal. In the current environment, a co-manager receives only 5 percent to 10 percent of the economics compared to 20 percent to 50 percent in the past. Therefore, most investment bankers are more incentivized to work on an M&A deal, because the fees are there. More money.

In addition, we have seen six to eight firms underwrite each of today’s deals. I believe companies should hire one firm as lead and between two to four co-managers, and give all participants the economics to incentivize them to develop a great deal. We have the investment banks that can provide research and trading support, but better deal flow and attractive economics are required to make the engines run.

Finally, the banking industry needs to make adjustments in pricing strategies. During my career, I have learned that the psychology of maintaining momentum is essential to complete a successful IPO. At pricing, the perception is that you need to price at least slightly above the range or revised range to prove it was a “hot” deal. Just look at all the headlines of recent IPO pricings and you’ll clearly recall who did well on day one.

Unfortunately, with some of the large IPOs that priced in 2012, the size of the deal and the price range was set too high. This has been problematic. It sets unachievable expectations and the deal becomes viewed as a failure and disappointment when it fails to meet those expectations. This is true not only for the IPO, but for a company’s early future as a public company.

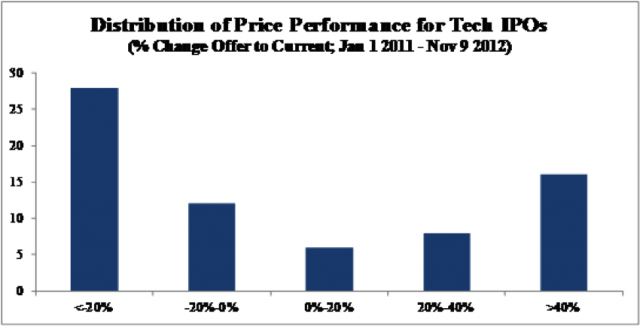

I believe not every deal needs to be huge and highly publicized, and changing our viewpoints toward this will help. We used to have a higher frequency of smaller-sized IPOs. In recent years, all the offerings have been viewed as either great or horrible, which creates a huge perception gap. It ultimately discourages institutional and individual investors alike from taking a position in a new IPO deal. But in the past, there was more of a bell curve and most IPOs were considered “moderately” successful and many went on to become great public companies. Today, we have a bimodal distribution.

The smallest category as we see in this chart is the “well-priced” deal, up modestly (up to 20 percent). Rather, the bigger categories are big winners or big losers.

Source: Dealogic

So what now?

While things are not going to change overnight, we can create a more fertile environment when the venture capital industry, investment banks and growth companies begin to collaborate and drive changes in the IPO ecosystem and get deals flowing again. My experience tells me it’s possible. I’ve seen it before, and it can happen again, at an even greater scale, to become the most robust IPO market in history. We have been complaining for years that the IPO market is dead, but with a few small tweaks, it’s here for the taking.

Sandy Miller is a General Partner with Institutional Venture Partners (IVP). He focuses on later-stage venture and growth equity investments in technology, Internet and digital media companies. He was recognized by Forbes Magazine as one of the top 100 venture capitalists in the world by his inclusion in all of the Forbes Midas Lists since 2007.